The most important strategic opportunities and risks for Stedin Group in 2022

This section contains an overview of our most important opportunities and risks, and a description of our top 5 risks. Our financial reporting risks are discussed in more detail in the ‘Judgements, estimates and assumptions’ section. For the risks concerning financial instruments, see the ‘Financial risk management’ section of the financial statements. For further information on the process related to strategic risks, see the ‘Risk governance’ section.

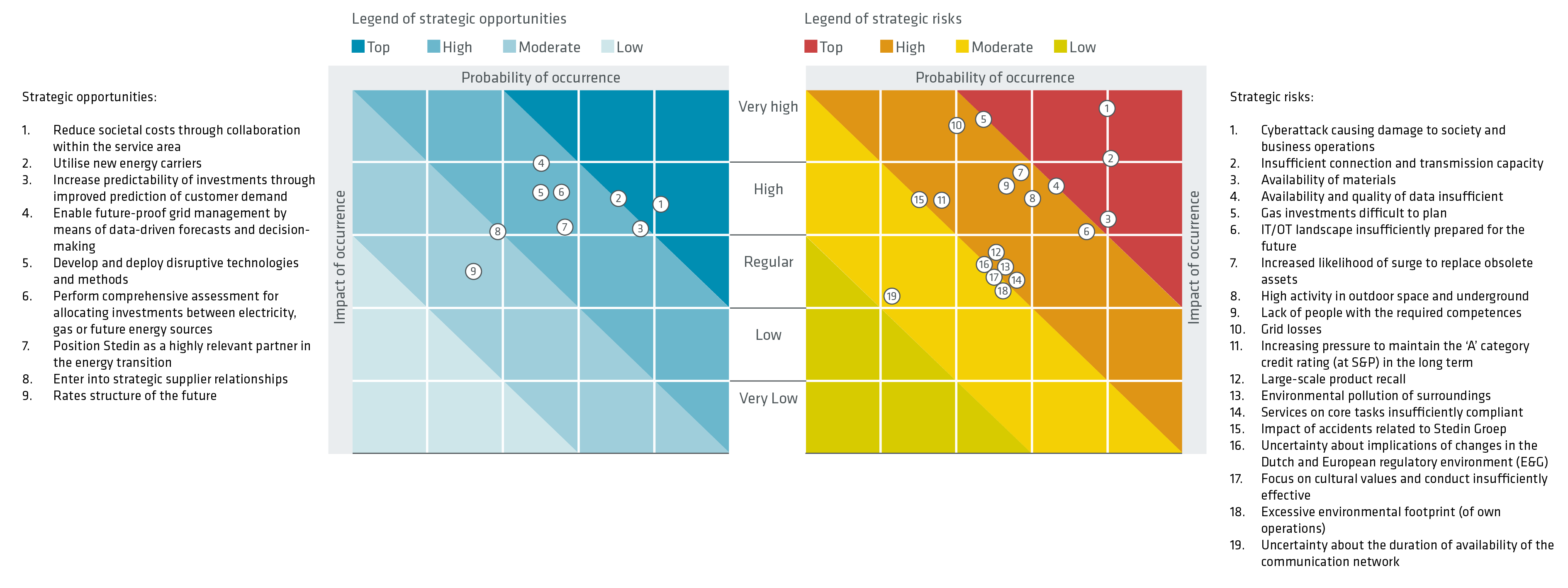

Connection of opportunities to strategic spearheads and material topics

Strategic spearheads | Development | ||||

|---|---|---|---|---|---|

Opportunity | Material topics |

|

|

| |

1 Reduce societal costs through collaboration within the service area | Affordable and efficient services - Financial and economic performance | ● | ● | ||

2Application of new energy carriers | Investments in infrastructure - Smart grids, data technology and innovation | ● | |||

3 Increase predictability of investments through improved prediction of customer demand | Investments in infrastructure - Stakeholder dialogue and environment | ● | |||

4Future-proof grid management based on data-driven predictions and decision-making | Smart grids, data technology and innovation - Security of supply | ● | ● | ||

5Development and deployment of disruptive technologies and methods | Smart grids, data technology and innovation | ● | |||

6Make comprehensive assessment in relation to investments between electricity, gas or future energy sources | Investments in infrastructure - Smart grids, data technology and innovation | ● | |||

7Position Stedin as a highly relevant partner in the energy transition | Stakeholder dialogue and environment - Smart grids, data technology and innovation | ● | |||

8Strategic supplier relationships | Stakeholder dialogue and environment - Impact on people and planet | ● | |||

9Rates structure of the future | Financial and economic performance - Affordable and efficient services | ● | ● | ||

+ New in 2022 / = Equal to 2021 / ↑ Increased relative to 2021 / ↓ Decreased relative to 2021

Connection of risks to strategic spearheads and material topics

Strategic spearheads | Change | |||||

|---|---|---|---|---|---|---|

Risk | Category | Material topics |

|

|

| |

1Cyberattack causing damage to society and business operations | Operational | Security of supply - Smart grids, data technology - Safety, security and cybersecurity | ● | ● | ● | |

2Insufficient connection and transmission capacity | Strategic | Customer satisfaction - Stakeholder dialogue and environment - Investments in infrastructure | ● | ● | ||

3Availability of materials | Operational | Security of supply - Investments in infrastructure | ● | ● | ||

4Availability and quality of data insufficient | Operational | Smart grids, data technology and innovation | ● | |||

5Gas investments difficult to plan | Strategic | Financial and economic performance - Affordable and efficient services | ● | ● | ||

6 IT/OT landscape insufficiently prepared for the future | Strategic | Smart grids, data technology and innovation | ● | ● | ||

7 Increased likelihood of surge to replace obsolete assets | Strategic | Security of supply - Investments in our infrastructure - Financial and economic performance | ● | ● | ● | |

8High activity in outdoor space and below ground | Operational | Investment in infrastructure | ● | |||

9 Unavailability of enough people with the required competencies | Operational | Investments in infrastructure - Good employment practice | ● | ● | ||

10network losses | Strategic | Financial and economic performance - Affordable and efficient services | ● | ● | ||

11 Increasing pressure to maintain the A- category credit rating (at S&P) in the long term | Financial | Investments in infrastructure - Financial and economic performance | ● | ● | ● | |

12Large-scale product recall | Operational | Security of supply - Impact on people and planet | ● | ● | ||

13Environmental pollution of surroundings | Compliance | Impact on people and planet | ● | |||

14Services on core tasks insufficiently compliant | Operational | Security of supply - Customer satisfaction | ● | |||

15Impact of accidents related to Stedin Group | Safety | Safety, security and cybersecurity | ● | |||

16 Uncertainty about implications of changing E&G laws and other regulations (NL and/or EU) | Compliance | Stakeholder dialogue and environment - Investments in infrastructure | ● | ● | ● | |

17Management focus on cultural values and conduct insufficiently effective | Strategic | Good employment practice | ● | |||

18Excessive environmental footprint | Strategic | Impact on people and planet | ● | |||

19Uncertainty about the duration of availability of the communication network | Operational | Smart grids, data technology and innovation | ● | |||

+ New in 2022 / = Equal to 2021 / ↑ Increased relative to 2021 / ↓ Decreased relative to 2021

The above table includes all the ‘Strategic risks and opportunities’ identified by us in 2022.

Categories of strategic risks and opportunities

Stedin Group assigns its strategic risks and opportunities to four categories, from ‘low’ to ‘top’. In evaluating risks and opportunities, we compare the likelihood of their occurrence with their potential impact on the achievement of our three strategic spearheads. This comparison led to the risk matrix below for 2022.

Risks are always changing, due to the multitude of uncertainties involved. We make periodic risk estimates, each time involving a reassessment of those factors to determine whether the risk is increasing, stable or decreasing. This applies both to the probability of a risk and to its potential impact if it does occur. We have identified several important developments compared with 2021:

The availability of materials poses a risk for Stedin. Unavailability of materials when they are needed can result in project delays. So far, Stedin has been able to ensure that the materials it needs are available when needed;

Due to geopolitical tensions, the costs of energy increased and also became more volatile in 2022. In addition, 2022 saw a sharp increase in costs for network losses. However, the measures taken have helped to mitigate this risk to a certain extent;

Since we signed the agreements framework with Alliander, Enexis and the national government, at the end of 2022, the pressure on maintaining our ‘A’ rating with S&P has decreased somewhat;

By scaling up our recruitment department, maximising our focus on the training of fitters and optimising the Strategic Personnel Plan, we are continuously improving our understanding of the challenge ahead of us while also expanding our resources to tackle it.

The matrix below shows the principal risks, expressed in terms of the likelihood of their occurrence and their potential impact on Stedin. The safety of our people and our environment is and will always remain one of our top priorities.

Risks

Below are descriptions of our top 5 risks.

Title of risk: | 1 Cyberattack causing damage to society and business operations |

|---|---|

Risk tolerance | Avoiding |

Risk assessment | Top |

Description: As a result of its strategic position as well as its social and economic importance, the Stedin Group infrastructure is an attractive target for cyberattacks. This is why cybersecurity is of fundamental importance to the continuity of Stedin’s activities. The chance of a cyberattack is progressively increasing as a result of technological developments and the increasing dependency on digitalisation. A cyberattack can have major consequences for the services of Stedin Group and its stakeholders. This can endanger vital infrastructure and hence the stability of the energy network. | |

Causes: State-sponsored actors: well funded and organised, whether or not directly related to foreign powers; their actions are inspired by political motives / Activist hackers (including terrorist organisations): their actions are inspired by political, social or other activist motives. Driven by their ideological motives, they carry out targeted attacks on Stedin due to its social relevance / Organised crime: actions are driven by economic motives. Employ ransomware or other means. Focus on personal data or improper financial transactions / Employees and suppliers: often able to access the internal network by virtue of their work. From this position, they can cause damage, intentionally or unintentionally / Inexperienced hackers: use a code published online to carry out attacks of a non-advanced nature. Competition between actors and particular interest in the topic of security play an important role in this regard. | |

Consequences: Discontinuity due to failures throughout or in parts of the infrastructure and loss of control over the supply of energy / Quality and efficiency of service provision decrease, and loss of control over own data and information systems / A cyberattack will slow Stedin down in implementing its role in the energy transition / Loss of control over switchgear can lead to serious personal injury / Very high repair costs: consequential loss for Stedin Group and society. | |

How did we respond to this fact: We are working on integral security that connects the related areas of expertise. Stedin applies a range of internationally recognised standards in order to reduce its vulnerabilities to outside threats, with a focus on prevention, timely detection and the resulting actions. Stedin has been designated a ‘critical service provider’ pursuant to the Network and Information Systems Security Act (Wet beveiliging netwerk en informatiesystemen (Wbni)), under the supervision of Radiocommunications Agency Netherlands. Of course, we are not immune to incidents. Fortunately, those incidents were small and did not result in a mandatory report under the Network and Information Systems Security Act (Wbni). In 2022, our ISO 27001 certification was expanded to include security of information in connection with the development, design, construction, maintenance, monitoring and administration of electricity and gas grids and the transportation of energy, with the appropriate support processes, systems, applications and resources. In its efforts to mitigate cybersecurity risks, Stedin can also rely on others. We collaborate with other grid operators within the Netherlands and Europe to increase the resilience of energy networks. We share knowledge and experiences with a variety of public and private sector organisations to pursue our strategic priorities and objectives. As a welcome side-effect of this, we are also contributing to digital security in the Netherlands as a whole. | |

Title of risk: | 2Insufficient connection and transmission capacity |

|---|---|

Risk tolerance | Neutral |

Risk assessment | Top |

Description: We plan the expansion of our electricity grids on the basis of customer demand forecasts. Timely reinforcement of our grids may not be possible if customer demand evolves much faster than expected or if execution takes much longer than planned. In that situation, we can offer our customers a connection but not the necessary transmission capacity and will be unable to meet the customers’ requirements. The customer must then modify, defer or cancel the planned project. The achievement of climate targets is also delayed if congestion management is not possible. Once congestion management is possible, a number of customers can still be connected. However, congestion management also entails certain costs. | |

Causes: The realisation of new infrastructure is a very time-consuming process. Planning permission procedures for spatial integration of the infrastructure take (much) more time than the project completion timelines of our customers. The feasibility of the energy transition is also a crucial factor for us. Combined with the substantial increase in the number of connection applications, this has resulted in large parts of the Netherlands turning into congestion areas. Since congestion levels within our service area have remained relatively low so far, developers have increased their attention to our service area. | |

Consequences: The ultimate consequence is that we will not be able to meet customer demand, or at least not in time. This means that customers will be required to either adapt, postpone or cancel their projects. In the end this may also block progress towards the climate targets, leading to reputational damage and potential claims by property developers and other parties. | |

How did we respond to this fact: It is important to have a clear view of expected customer demand for grid capacity and connections. This enables us to identify potential bottlenecks in the grid, to make timely provisions for the required expansion of our grid and to address issues in collaboration with customers. For example, we consider parts of our grid that do still offer sufficient capacity or that would enable us to spread demand for capacity more evenly over time. We also use a number of technical solutions, such as the so-called failure reserve, or capacity-switching to ease the pressure on bottlenecks. In the latter case, for example, we engage in dialogue with customers that want to provide flexibility. We have gained considerable experience with this approach in the Zuidplaspolder, where commercial growers use their CHP installations to provide flexibility. We use the Regional Energy Strategies (RES) to provide insight into the available grid capacity, including scheduled grid reinforcements for our RES partners. And we use our ‘opportunity maps’ to show our customers and stakeholders where new initiatives are most likely to be implemented. This provides public authorities with clarity regarding the feasibility of the RES ambitions. In the years ahead, Stedin will continue its investments in improving the transparency of available and scheduled grid capacity levels. In addition, we endeavour to reduce the completion times for new infrastructure by speeding up the spatial integration of our new grids. For this purpose, we engage in early-stage consultation with our stakeholders. Together with fellow grid managers, moreover, we proactively lobby for an expansion of connection options. This has already resulted in the so-called ‘opknipverbod’ (a prohibition of multiple connections) and cable pooling. In addition, the adapted congestion management method has come into force, enabling grid managers to connect more customers. | |

You can read more about the impact of this risk in the ‘Stakeholder dialogue and environment’ and ‘Investment in infrastructure’ sections. | |

Title of risk: | 3Availability of materials |

|---|---|

Risk tolerance | Neutral |

Risk assessment | Top |

Description: In the event of material shortages, we may be forced to slow down the implementation of grid adaptations and would thus become a limiting factor in the energy transition process. The principal objective is to further solidify supplier relationships for services and materials, to ensure the latter are available when we need them. | |

Causes: The past few years have seen repeated disruptions of demand and supply on the supplier market (due to COVID-19, the war in Ukraine and tensions between China and Taiwan, for example). Geopolitical developments in 2022 resulted in exceptional external circumstances on the supplier and commodity markets. High levels of uncertainty about global prices of production, transport and raw materials (at Tier 2 and Tier 3 level) among our suppliers and soaring inflation rates have led to considerable uncertainty about the availability of materials. Despite the current challenges on global supplier markets, Stedin actually intends to considerably increase its efforts to build the infrastructure for the energy transition in the years ahead. | |

Consequences: With reduced levels of availability, the prices of materials may increase sharply and Stedin’s overall activities may become more expensive to perform. Work schedules may also come under pressure. | |

How did we respond to this fact: We took three mitigating measures. The most relevant preventive measures are the following: (1) designing a data-driven method to create an enhanced demand forecast system for 2023 and periodic forecast updates, so that we can order materials earlier if necessary, (2) determining and recalibrating optimum stock levels, and (3) measuring and improving supplier performance. | |

Title of risk: | 4Availability and quality of data insufficient | |

|---|---|---|

Risk tolerance | Avoiding | |

Risk assessment | Top | |

Description: Stedin’s historical data policy combined with increasing demand for our data from our environment may cause the availability and quality of that data to be insufficient. In that case, the data cannot be used as an asset, potentially resulting in insufficient levels of management and asset information. This, in turn, may jeopardise the security of our operations and prevent us from achieving our strategic objectives. | ||

Causes: Historical data policy / Low priority for data management within Stedin / Increased customer demand for data. | ||

Consequences: Process inefficiencies / Inability to use data as an asset / Management information of insufficient quality / Failure to achieve improvements and to ensure continuous improvement / Non-central, local solutions for substandard data quality (which is an inefficient and non-future-proof approach) / Data-driven grid management infeasible. | ||

How did we respond to this fact: We improve the quality of our asset data by implementing a variety of data improvement projects. These projects are included in the strategic improvement plan. This year we completed the smoke-testing and updated the associated data sets of 22,000 medium-voltage installations. We also ran smoke tests of a considerable part of our low-voltage cabinets; the remainder will follow in 2023. We launched new projects to ensure the quality of public lighting data, especially on aspects such as contact safety and low voltage in the Zeeland service area. This had to do with a scheduled data integration. These data improvements are essential to ensure optimal utilisation of the asset data. In addition to improving the quality of our asset data in projects, we have also launched a programme to improve newly recorded data in our operational management. The chain structure also means that the focus on data quality in operational management has increased. Revision processing (recoding adaptations to the grid) in particular is seeing significant improvements. The new geographic information system (GIS) and Mobile Workforce (GIS app for fitters), implemented in late 2023 and early 2024, signify another major step forward. In addition, we worked on extracting data from developments at our customers, including housing associations, municipalities and power generation companies. For housing construction forecasts, for example, we look at actual numbers built, planning permission granted and long-term forecasts from the various perspectives. This enables us to continually improve our estimates. We also extract valuable data from customer demand for additional capacity. By using that data we continually enhance our insight into our grids. Among other things, this has resulted in a congestion management dashboard. In addition, we have developed several models which provide data-based insight into our future grid capacity and quality, allowing us to make more targeted investments. This also provides insight into the data improvements necessary for even more reliable results. | ||

You can read more about the impact of this risk in the ‘Smart grids, data technology and innovation’ section. | ||

Title of risk: | 5Gas investments difficult to plan |

|---|---|

Risk tolerance | Neutral |

Risk assessment | Top |

Description: Since we are unable to plan for the energy transition in the best possible way and only have limited space below ground, there is a risk that the necessary gas-related investments are underestimated and turn out to be higher than expected. | |

Causes: Inability to optimally plan for the energy transition / Limited space below ground. | |

Consequences: Higher investments and costs than estimated in the Strategic Investment Plan. | |

How did we respond to this fact: Active lobby within Netbeheer Nederland to minimise the impact of EU legislation on methane emissions (initial impact 20-fold work package) / Prepared a Master Vision for Gas formulating a vision for gas based on developments and identifying the interventions required / Construction of heat grids (and possibly other infrastructure) affects our own gas infrastructure, forcing us to either reposition or replace our gas grids. We identified where this might be an issue and how we might be able to influence this, focusing mainly on municipalities / More stringent requirements of municipalities result in higher gas infrastructure construction costs due to the measures to be implemented; we are in consultation with the municipalities on this issue, particularly with the municipality of Utrecht / By focusing on innovations such as green gas and hydrogen, we can identify where and how the gas grid can be reused and will continue to be required after 2050. | |